NEW YORK—Starbucks Corp. executives laid out an ambitious financial roadmap through fiscal 2028 at their first investor day under CEO Brian Niccol, signaling confidence in the “Back to Starbucks” transformation plan a year after its launch. CFO Cathy Smith, speaking to CNBC , emphasized the timing: “We set the Back to Starbucks plan a year ago… it’s clear now we’re seeing the momentum and the plan is working.” The event highlighted transaction-driven sales growth, $2 billion in targeted cost savings, and a pivotal China joint venture, even as near-term earnings face headwinds from investments and commodity pressures.

In the first quarter of fiscal 2026, Starbucks reported global comparable store sales up 4%, with U.S. comps matching that figure on 3% transaction growth and 1% higher average ticket, per the company’s Q1 earnings release . This marked the first U.S. transaction increase in eight quarters. For full-year 2026, management guided to global and U.S. comp sales growth of 3% or better, non-GAAP EPS of $2.15 to $2.40, and 600 to 650 net new stores globally. Consolidated net revenues rose 6% to $9.9 billion in the quarter, though non-GAAP EPS of $0.56 missed estimates amid labor and remodel investments.

Turnaround Momentum Builds on Transactions

Smith underscored the durability of 3% comps as a baseline for Starbucks’ scale: “3% comp is a really good comp for our size scale and our global nature… underpinned by transactions.” Q1’s 4% global comp reflected 3% traffic gains, reversing prior declines. Executives attributed this to Green Apron Service rollout, which boosted peak throughput to under four minutes in cafes and drive-thrus, according to the Investor Day press release . COO Mike Grams noted: “Great execution creates better experiences, which drives repeat visits and fuels growth.”

Menu innovations and brand marketing form demand drivers, with new espresso, matcha, chai, and Energy Refreshers slated for 2026. A reimagined Rewards program launches March 10 with Green, Gold, and Reserve tiers, faster star earning, non-expiring stars for higher levels, and perks like free monthly customizations—driving nearly 60% of U.S. sales. Chief Brand Officer Tressie Lieberman said: “We’re not chasing trends. We’re building on a beloved platform.”

Store uplifts, costing $150,000 each versus prior multimillion-dollar remodels, will add 25,000 U.S. seats by year-end 2026, per Reuters . Plans call for 400 net new U.S. company-operated stores annually by 2028, targeting 5,000 additional long-term opportunities.

Margin Push Prioritizes Savings Over Pricing

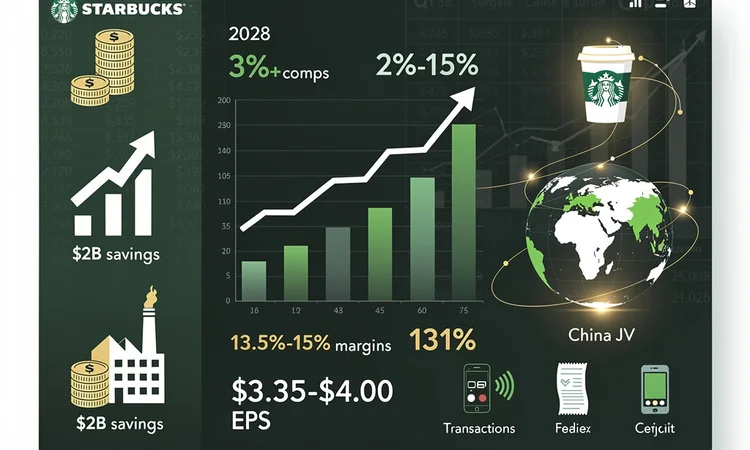

Starbucks targets non-GAAP consolidated operating margins of 13.5% to 15% by fiscal 2028—pre-pandemic levels—via 5%+ annual revenue growth, 3%+ comps, 2%-3% from new stores, and over $2 billion in cost savings. Smith clarified to CNBC: “Margin growth is first going to come from probably not pricing for us. Pricing is going to be our last lever.” Value scores hit all-time highs across age groups, enabling selective inflation-linked hikes.

Cost discipline spans 90+ initiatives, including cheaper remodels, supply chain fixes aiming for 90% daily resupply by 2026 end, and AI tools like Green Dot Assist for drive-thru order-taking and automated counting. Smith added: “Technology can do the work in the background… preserve that customer-barista connection.” International margins, 13% in fiscal 2025, eye high-teens post-China shift, per CNBC coverage.

Fiscal 2028 non-GAAP EPS guidance stands at $3.35 to $4.00, with over 2,000 net new global stores. Smith told investors: “Starbucks has enduring strengths and we are building on them. Our financial framework shows how we will translate our ‘Back to Starbucks’ strategy into sustainable, profitable growth.”

China Venture Trades Earnings for Acceleration

China, with 8,000 stores in tier-one and two cities, faces a joint venture with Boyu Capital closing Q2 2026, granting Boyu up to 60% stake at a $4 billion enterprise value—total business worth over $13 billion including Starbucks’ 40% retained interest and licensing fees. Smith noted to CNBC: “We’re really optimistic about China long term… our capital partner has bigger growth expectations” to offset modest dilution, potentially 15 cents to 2028 EPS under current plans.

The asset-light model mirrors McDonald’s, enabling expansion into tier-three-plus cities toward 15,000-20,000 stores, doubling international footprint to 40,000. International CEO Brady Brewer affirmed: “The role of our international business is very clear. We are an asset-light growth driver.” Forecasts assume ongoing China retail operations, with JV upside for higher growth.

Beyond 2028: Supply Chain, Units Fuel Upside

Smith highlighted post-2028 levers: “We still have work to do in our supply chain… as we build new coffee houses with a better cost profile.” Even at 400 annual U.S. openings against a 10,100-store base, improved economics will gradually lift P&L. Niccol affirmed: “This is just a waypoint… ambitions extend well beyond this timeline.”

Q1 results and guidance reflect abating coffee volatility and tariffs, with prices rolling through inventory but maintaining value. Smith said: “Coffee prices should be coming down… our coffee prices in the coffee houses to our customers are at a great value.” Shares have risen 15% in early 2026, outperforming peers, though profitability lags amid investments, as noted in U.S. News .

The roadmap positions Starbucks for sustained growth, blending operational rigor with innovation. As Smith concluded on CNBC: “The first one is always going to be on topline… if we keep doing the right things, having a great customer experience.” Investors await execution amid consumer pressures and competition.

Leave a Reply

Your email address will not be published.